The OECD study examined shows that in Italy both the number of doctors, which is decreasing (about 4 per 1,000 inhabitants), and their age, which is increasing, are worrying. In fact, more than half are over 55 years old. On average in 2000, about one fifth of doctors in OECD countries were over 55 years old, while the ratio increases in 2019, a period in which it rises to more than one third (OCSE – State of Health in the EU – Italy).

As for nurses, on the other hand, in 2019 Italy ranks below the OECD average, counting about 6.2 per 1,000 inhabitants when the OECD average is 8.8. There are more nurses than doctors in most of the OECD. On average, there are just under three nurses for each doctor (according to international standards) while in Italy they are 1.5 (OECD Indicators – Health at a Glance 2021).

Fewer and fewer doctors but digitalization is taking hold

According to the Italian Public Accounts Observatory, Italy with over 1,400 inhabitants per general practitioner (therefore in November 2021 the figure has worsened), suffers from a lack of primary care in the area compared to the major European countries. Furthermore, there are considerable differences between regions: in the North, general practitioners have a higher load of clients than in the South (Article Repubblica – Mancano medici di base: Italia sotto la media Ue. E con il turnover il problema crescerà).

In the various Italian regions, the digitization of the health system is proceeding at different rates.

In 2016, the Digital Health Agreement was reached to manage and promote the dissemination of e-Health in a coordinated way throughout the territory. The main priorities were:

- the development of electronic health records (EMR),

- telemedicine systems and ICT innovations that can improve management

- experience of patients’ workflow.

The Strategy for Digital Growth and the Three-Year Plan for Public Administration Information Technology 2019-2021 was created to drive the digitalization of the public health system. This three-year plan includes initiatives that will further promote the implementation of EMR, e-prescriptions and telemedicine in all regions (Ministry of Health, 2017).

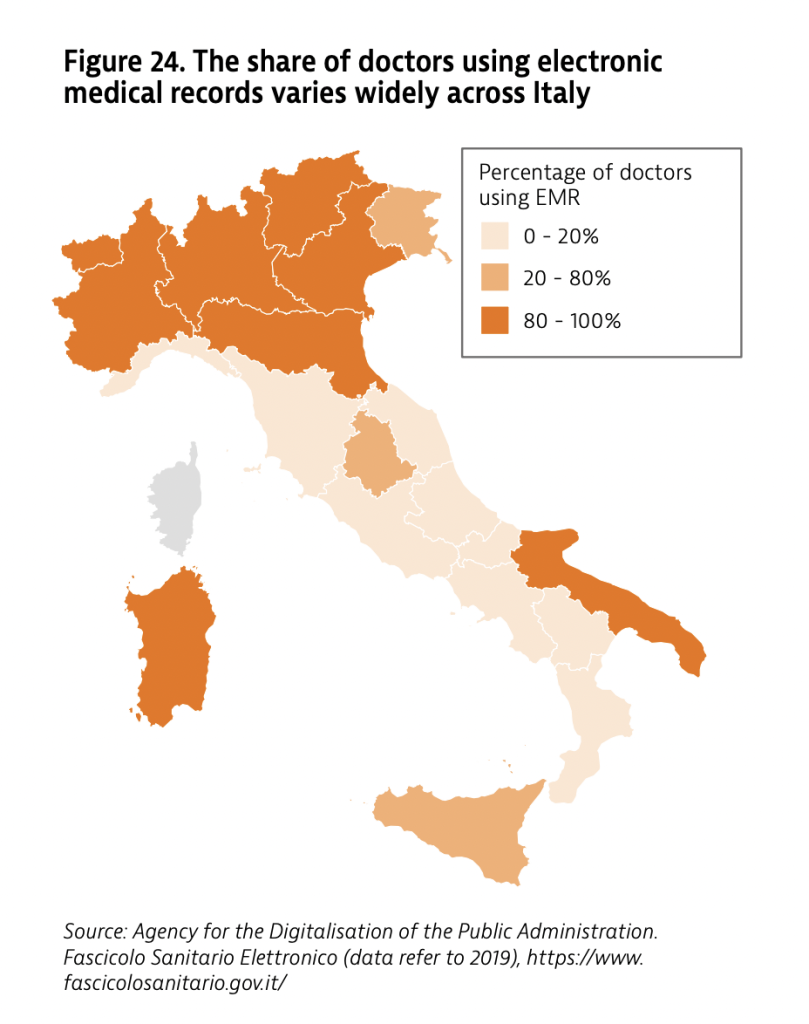

The regional spread of EMRs in Italy still varies considerably.

Although no doctor had ever used EMRs in seven regions in 2019, in eight regions more than 80% of doctors used them (State of Health in the UE – Italy – OCSE, Figure 24).

From this we can deduce that digitalization allows a more agile patient management. Looking only at Italy in the Northern regions, general practitioners who have switched to digitalization are able to support the greater load of patients compared to those in the South.

We are witnessing a radical change, even medicine is going virtual.

It is a trend, of which only the first movements are seen, but knowing how to identify them in time will allow you not to be left behind.

An unexpected event: the pandemic

Having health data, documents and information in a timely and accurate manner ensures safe, effective, responsive and patient-centered care. Care also becomes affordable and accessible if data and information are accessible to decision makers (patients, healthcare professionals, managers or scholars). New digital health services built with the use of new technologies such as Artificial Intelligence (AI), Machine Learning, Neural Networks, Intelligent Algorithms or IoT, can lead to better access to healthcare and greater patient satisfaction. A digital transformation of healthcare in OECD countries is underway, accelerated by the COVID-19 pandemic and driven by the digitization of information infrastructures, as well as increasing patient demand.

COVID-19 accelerated the trend (OECD Indicators – Health at a Glance 2021).

According to a McKinsey & Company study updated in July 2021, 64% of doctors surveyed said they were more confident in using virtual care after the pandemic than before.

Additionally, healthcare professionals quickly scaled back offers and reported seeing 50 to 175 times the number of people using telemedicine visits than before the pandemic began.

The increased use of virtual care by both healthcare professionals and patients shows the role that virtual care can play in rebuilding a highly fragmented healthcare system.

Not long ago, a patient’s medical record was not shareable between primary care providers and specialist care providers. This lack of visibility has led to a series of problems for the patient (from drugs to often contradictory health guidelines, etc.). Today, virtual care platforms not only enable the sharing of data between healthcare professionals, but also the collaboration of care teams.

McKinsey’s own study estimates that up to $ 250 billion in health care spending in the United States could be shifted to virtual or virtually enabled care.

About 40% of US consumers surveyed said they believe they will continue to use telemedicine in the future, compared with 11% of consumers who used telemedicine before COVID-19.

It also shows that between 40 and 60 percent of users express interest in a broader set of virtual health solutions, a virtual health plan (Article McKinsey & Company – Telehealth: A quarter-trillion-dollar post-COVID-19 reality?).

Trend acceleration

With the onset of the COVID-19 pandemic and the resulting restrictions on mobility, work and social interactions, many more people have been unable to receive in-person medical advice. In 2019, before the pandemic, remote counseling by phone or video accounted for less than 10% of all consultations in Australia, Finland, Lithuania, Norway and Slovenia. Since the start of the pandemic, the percentage of adults who have reported having an online or telephone medical consultation has increased significantly and by mid-2020, nearly one in three adults had used a remote consultation, a percentage that had risen to nearly one in two by early 2021. Countries where the use of remote consultations was highest in mid-2020 also experienced higher growth rates between mid-2020 and early 2021. (OECD Indicators – Health at a Glance 2021).

In the last year we have seen the greatest digital acceleration the healthcare sector has ever known. A revolution, forced by the pandemic, in consumer attitudes towards the adoption of digital health care and in the way in which the market must respond. Like never before, we need to keep up with the pace of this change.

A new research entitled “Digital Frontiers – The Heightened Customer Battleground” commissioned by VMware to explore the links between technological innovation, people and society and conducted on more than 6,000 consumers in 5 countries found that almost half of Italian consumers (45%) feel comfortable replacing medical classic consultations with remote virtual appointments (44% at European level). And this does not only concern the younger generations, users between 45 and 54 have been among the most enthusiastic about the idea of a new virtual world of healthcare.

The pandemic has changed the dynamic that pushes the user to relate to virtual health services.

Let’s take the UK as an example: before the virus, video appointments made up only 1% of annual visits (€ 340 million) with doctors and nurses from the British National Health Service. But as the epidemic accelerated, when the NHS (National Health System) encouraged all 7,000 UK doctors’ offices to cut down on face-to-face appointments, we have seen physical visits decrease by 57% compared to the previous year, while online medical platforms have seen a 70% weekly increase in consultations.

The pandemic has forced many to overcome concerns about the safety of virtual meetings with doctors. Today we all accept much more easily the idea of a 10-minute video call (telemedicine) to have a discussion on any exam done rather than going to the doctor and waiting for their turn in a waiting room together with other patients.

The world is changing and the pandemic is accelerating the change. Digitization is everywhere and it is easy for the user to extend its use to the healthcare sector as well. The habit of new technologies in sectors other than healthcare leads the patient to expect that healthcare is also immersed in digital technology.

All this means that we are faced with a great opportunity. This is the time to build a modern, advanced and safe healthcare system to meet the expectations of healthcare users in cost, quality and provision of patient care. The new technology-based world of healthcare is here, we just need to make it happen (Article VMware – “Il mondo nuovo” della tecnologia per l’healthcare).

The VMware’s study aims to better understand how technology can help companies improve customer experience and services and highlights that, despite last year’s digitization efforts, organizations are failing to meet their customers’ digital expectations, who feel largely disappointed.

According to the research, the healthcare market in Italy in particular has failed to deliver cutting-edge digital experiences. These experiences could include the introduction of virtual reality and augmented reality. And 83% of respondents define themselves as “digitally curious” or “digital explorer”, confirming a high propensity and receptivity towards digital.

The data that emerged should represent both a warning and an opportunity for companies: 52% of consumers say that they would be ready to move to the competition if their digital experience did not live up to expectations and only 8% would remain faithful. . And 60% would abandon a site or app if they couldn’t fix a problem immediately – whether through a chatbot, live chat, or directly over the phone. The ethical choices of a company also weigh in the choice of consumers: 48% of respondents would stop buying products from companies that do not publicly share their ethical policies (Article VMware – I consumatori italiani insoddisfatti delle loro esperienze, nonostante il grande “digital switch” del 2020).

According to the Digital Frontiers research, presented by the VMware foundation, Italians demonstrate a high level of confidence in new technologies in the healthcare sector, especially if they can demonstrate that they can improve their daily lives.

In the United States, 14.1 billion dollars were invested, or about 40% of the entire share of funding raised by healthcare startups in Q2 2021, precisely in those startups operating in the digital health sector.

Even in Europe, the value of healthtech startups has increased fivefold in 5 years: 41 billion dollars in 2021 compared to 8 billion in 2016.

The digital healthcare market in Italy was worth around 3 billion euros in 2020 and is expected to reach 4 billion by 2024.

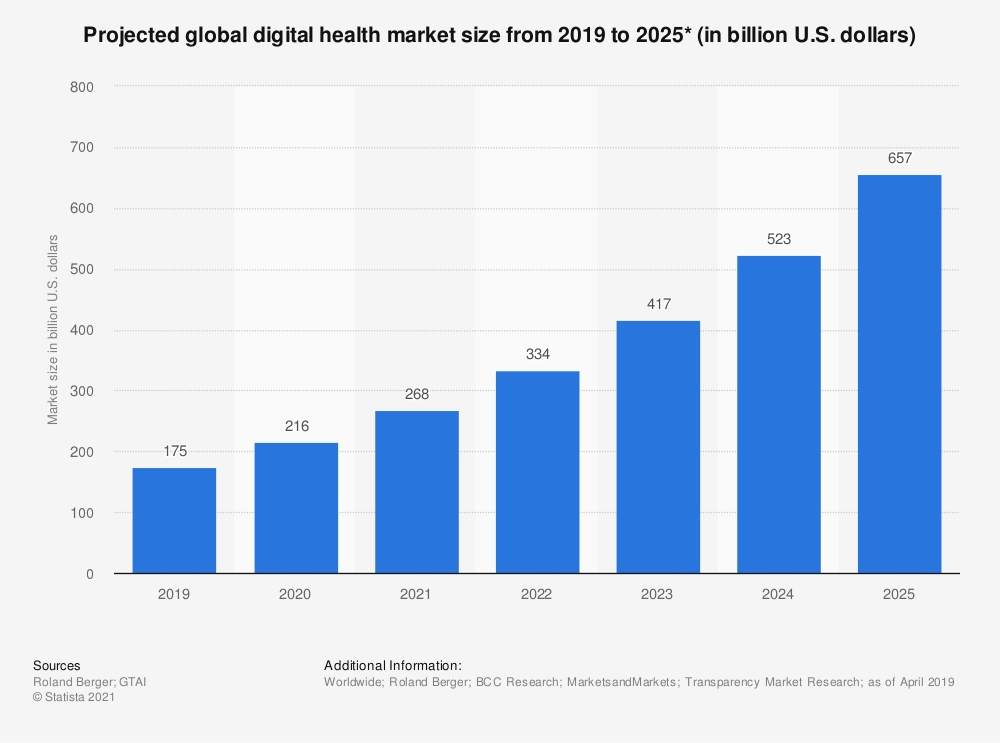

It is estimated that – in 2025 – the value of the global digital health market will be around 657 billion dollars (it was worth 175 in 2019) (Article HealthTech360 – Digital Health: investimenti record anche nel 2021).

Zion Market Research evaluates the global market of m-Health apps (mobile Health or the part of e-Health that concerns the services that are carried out through the use of mobile and wireless devices such as smartphones and tablets) about 8.0 billion dollars in 2018 and expects to generate approximately $ 111.1 billion by 2025, with a CAGR of approximately 38.26% between 2019 and 2025 (Article Zion Market Research – Global mHealth Apps Market Will Reach USD 111.1 Billion By 2025: Zion Market Research).

The COVID-19 emergency has certainly increased awareness among citizens, health professionals and managers of health facilities on the crucial contribution of digital technology in the process of prevention, treatment and assistance. But a full evolution of the Italian health system towards a connected and personalized health system is still a long way off, thanks to a mature use of digital technologies.

Digital Innovation in Health Observatory of the School of Management of the Politecnico di Milano which also takes stock in its latest report on e-health expenditure which, in 2019, had grown by 3%, reaching a value of 1.43 billion euro and confirming the growth trend already observed in recent years. Growth in investments for digital health in general is expected in 2020.

The boom in interest in Telemedicine during the lockdown has led to an increase in experimentation: 37% of health facilities are experimenting with Telemonitoring (27% in 2019) and 35% in Televisit (15% in 2019).

Even doctors are more interested in e-health: for 57% of specialist doctors and 50% of general practitioners (GP) there will be a significant impact on the health system in the next five years of Digital Therapies, technological solutions to optimize patient care (either together with or independently of drugs, devices or other therapies). Doctors already recommend health apps to their patients, including those to improve physical activity (44% of specialists and GP), those to remember to take a drug (36% specialists and 37% GP) and those to remember to take a drug (36% specialists and 37% GP) to monitor clinical parameters (35% specialists and 40% GP).

Citizens are also increasingly familiar with new technologies. During the health emergency, 71% of those who needed to find out about correct lifestyles did so on the web and 79% want to do so in the future. 74% are interested in doing so to seek information on health problems and diseases and 73% are interested in drugs and therapies. The most used health apps are to test mental skills (28%), to increase physical activity (23%) and to improve nutrition (14%). The use of chatbots and voice assistants for the self-assessment of symptoms is more limited (10%).

Mariano Corso, Scientific Director of the Digital Innovation in Health Observatory, affirms that to make our National Health System more resilient in the face of a new health crisis, it is necessary not only to strengthen the system on the territory, but to change its architecture towards a model of care connected in which the organization, the care and assistance processes are rethought from a digital point of view. There is ample room for improvement, the digitalization of healthcare is still insufficient in many areas that could have alleviated the social, economic and health cost of the pandemic and which could make a difference in the future, such as Telemedicine, Apps for the patient, Digital therapies and Artificial intelligence.

One in four citizens monitors the data collected through an App or wearable device, using it to make decisions about their lifestyle. 10% view them but do not use them, because they are not reliable (7%) or difficult to interpret (3%). Only 5% share them with the doctor, 67% did not do so because they did not need it and 13% because the doctor was not interested in receiving them. Yet, medical specialists are interested in receiving data on clinical parameters (51%), adherence to therapy (48%) and symptoms (42%) of their patient, and also general practitioners, especially on clinical parameters (30%) and adherence to therapy (26%).

The Milan Observatory has registered 302 startups at an international level that offer services and applications in the health field for patients, which receive an average funding of 6.8 million dollars. The most funded are those that improve physical activity (€ 21.6m), nutrition (€ 18.5m), women’s health and pregnancy (€ 12.7m), those that reduce stress and promote mindfulness (€ 11.4m) and facilitate doctor-patient interaction (€ 9.6m). Below average, however, are the solutions for monitoring vital parameters (€ 3.3m) and adherence to therapy (€ 2.8m).

Chiara Sgarbossa, Director of the Digital Innovation Observatory in Health, says that the doctor’s role will be fundamental in advising the patient on the application that will be a valid support for the patient and in allowing the doctor to receive useful data for treatment and support. And she stresses that the real challenge will be the integration of this data into the computer systems used by doctors, health facilities and regions (Article Corriere – E-health, il 50% dei Cio italiani stima investimenti in crescita).

“Now all the players in the Italian health ecosystem, from doctors to patients, from institutions to health facilities, are called upon to collaborate to build a” connected “healthcare modeled on the needs of the citizen / patient.” (Article Sole24Ore – La telemedicina in Italia: cosa è successo durante l’emergenza e cosa fare? Sei azioni per la Sanità del futuro).

Healthcare and Artificial Intelligence

According to a study by Frost & Sullivan, a Californian consulting firm that deals with market analysis and support in strategic growth, in 2021 the market for Artificial Intelligence applied to the healthcare sector should be worth something like 6.6 billion dollars. By 2025, the healthcare market linked to artificial intelligence will be worth something like 193 billion dollars. Innovation in healthcare will allow for better care, cost cuts and greater organizational efficiency.

In recent years, we have moved from paper to digital archiving. Patient monitoring and screening devices have also gone digital. This change has allowed the entry of Artificial Intelligence also in healthcare, for which today data is used and processed in an optimized way only with technologies based on Artificial Intelligence to increase the efficiency and accuracy of data reviews and to reveal schemes underlying the collected data that can be used to improve the analysis. Furthermore, they can highlight inefficiencies and simplify procedures, both from a clinical and an operational point of view.

The margins for improvement in the healthcare sector are enormous, but the problems of change linked to the safety and operational functioning of the structures, which do not always allow for the easy introduction of new technologies, are equally high. In all sectors, Artificial Intelligence applications must be designed for the specific sector, in healthcare in particular this is more valid than for other sectors. And, possibly, be within the reach of populations around the world. For this reason, investments continue to grow: ad hoc paths are needed for each individual need and, to develop them, time and money are needed (Article PICTET: eHealth: il legame tra Intelligenza Artificiale e sanità è sempre più stretto).